The initial dip following the Advanced Micro Devices (AMD) Q4 results tells the main part of the story for the stock. Both bulls and bears will like the report, but the long-term story still favors the bulls. The investment thesis remains bullish as the chip company moves to capture market share in 2020 and beyond while the market desires higher growth rates exiting the year.

Image Source: AMD website

Predictable Mixed Numbers

AMD recently surged to an all-time high above $52 on the backs of expected record setting Q4 results. The company delivered 50% revenue growth and EPS growth of 300%, but the chip company didn’t beat expectations by any wide margin giving the bears something to latch onto.

Even the breakdown of the two reported segments left a lot mixed feelings. The computing division smashed estimates while the server segment missed estimates by nearly $150 million despite supposed strong Epyc 2 processor sales.

- Computing and Graphics: $1.66B vs $1.50B consensus

- Enterprise, Embedded and Semi-Custom: $465.0M vs $603.8M

The numbers were even more perplexing considering the big $800 million data center revenue beat by competitor Intel (INTC). The same division for AMD only generated quarterly sales of $465 million including other non-server sales while Intel had sales of $7.2 billion.

Ryzen and Radeon processor sales continue to deliver for AMD with sales up 30% sequentially. Those chips generated the majority of the impressive $405 million in operating income in the quarter.

The general disappointment is Intel being able to claim so much additional data-center revenues while AMD had the market- leading Epyc 2 chip. Still, a lot of the financial results were impressive with gross margins hitting 45% for the highest level since 2012 and positive free cash flows leading to the strongest net cash position in years.

Last year, AMD ended Q4 with net debt of $94 million. This year, the company ended December with net cash of over $1.0 billion for an improvement of $1.1 billion in the last 12 months. The net cash position is the highest since 2006.

Don’t Stress Guidance

One of the reasons AMD traded down 5% in initial trading was the disappointing Q1 guidance despite the solid full-year numbers. The market always heavily weights the near-term numbers over any longer projections.

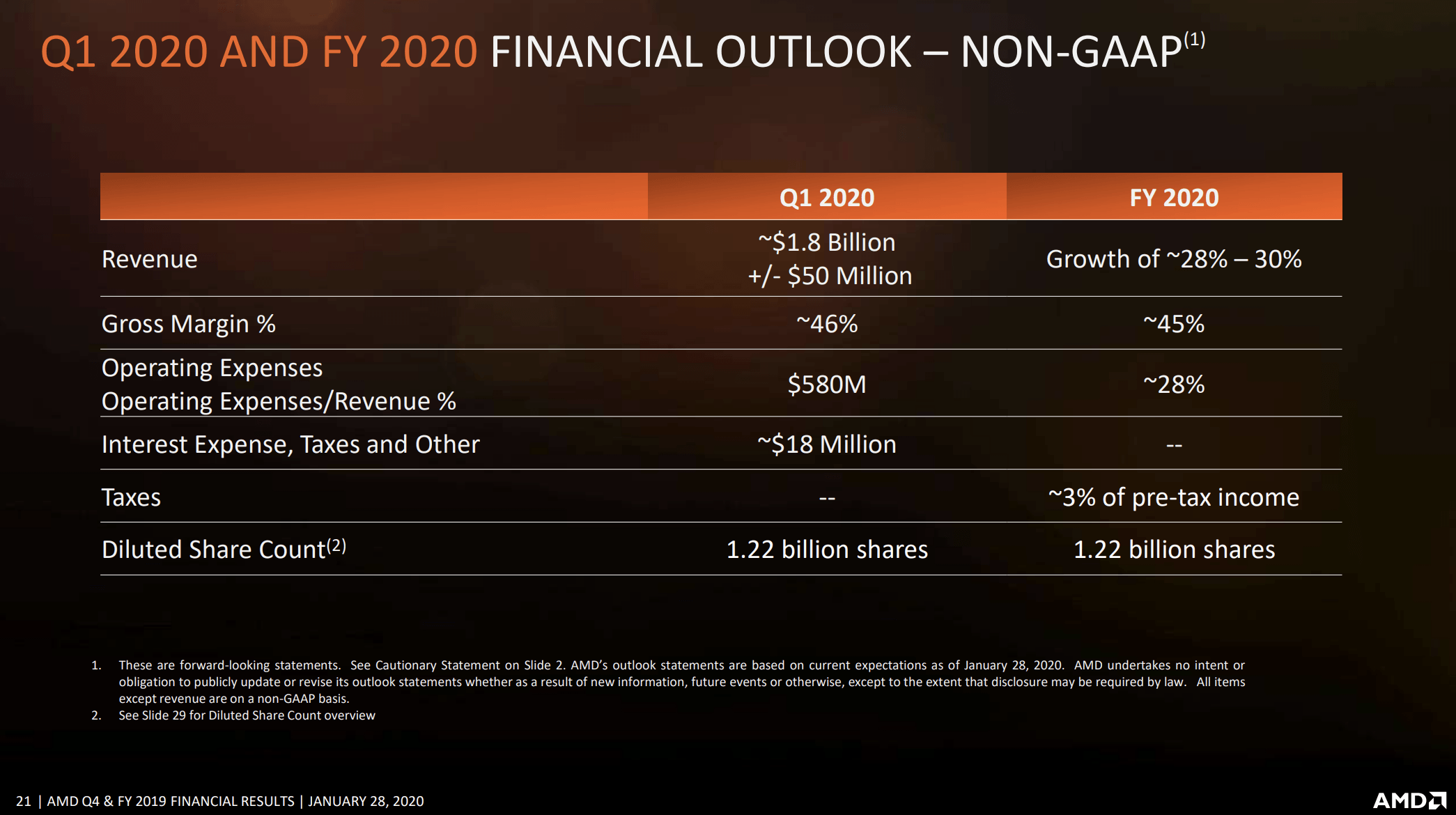

AMD has a tendency to disappoint in the short term while still making strong progress on the long term. The Q1 revenue guidance of $1.8 billion fits into that category with forecasted growth of over 40%, but still missing analyst estimates for revenues of $1.86 million.

The 2020 guidance is more inline with expectations with revenue growth of 29% leading to total sales of $8.68 billion versus consensus analyst estimates down at $8.59 billion. AMD will both generate strong annual growth and beat analyst targets in the year.

Digging into the above 2020 financial targets, the chip company provided the following basic numbers:

- Revenue: $8.68B

- Gross Margin: $3.91B

- OpEx: $2.43B

- Operating Income: $1.48B

- Net Income: $1.44B

- EPS: $1.18

The general EPS target tops analyst estimates now in the $1.12 range. While the revenue forecast has a near $2.0 billion boost from the 2019 levels, the company isn’t forecasting much improvement for the Q4 numbers exiting the year. AMD expects substantial gains in the server and semi-custom markets during the year, but the actual revenue numbers aren’t lining up.

The numbers are very conservative in several areas. The Q4 gross margins were already at 45% and the guidance for Q1 is at 46%. The company would have to take a gross margins hit in the 2H of the year, though the potential for lower margin sales from semi-custom revenues could provide a drag on gross margins.

The operating expenses were down to 26% in the last quarter with guidance forecasting a 200 basis point hit for 2020 despite the higher revenues. The opex guidance at 28% of revenues appear high considering the lower costs from the console revenues due to the console makers contributing a substantial portion of the R&D expense.

The analysts generally share the same concern about the 2020 guidance and how the numbers will play out during the year. AMD suggests limited revenue growth in Q4 considering console growth should drive semi-custom revenues in the range of the current consensus revenues gains of only $320 million to reach $2.45 billion.

In fact, Stacy Rasgon from Bernstein Research had the following question on the earnings call pointing out how easy AMD should beat their 2020 guidance despite the appealing headlines of 28% to 30% revenue growth:

if I sort of squint at the second half, it seems to me you are probably guiding it implicitly call it $800 million to $1 billion over the second half of 2019. How much of that you think is console versus non-consoles, because it’s not hard to get a console number, especially in the beginning of a ramp that’s not that far off that number, which doesn’t leave all that much room to ramp the rest of the business? So is this just conservatism or like what else are you expecting here?

One can easily foresee the server market and console market each seeing YoY growth for Q4 revenues far in excess of the above $320 million projected revenue growth. Even with PC sales weakness in the 2H of the year, AMD shouldn’t see sales declines in the Computing & Graphics segment due to strong Ryzen and Radeon sales.

The company is positioned to beat the guidance which already forecasts EPS to nearly double the $0.64 earned in 2019. The ultimate $10 billion revenue target is still achievable and might roll into 2021 as long projected.

Investors should watch for the margin story as AMD tends to exceed their guidance more on margins than revenues. Below is the updated financial targets for when the chip company reaches $10 billion in revenues:

- Revenue = $10.0 billion

- Gross Margins @ 50% = $5.0 billion

- OpEx @ 25% = $2.5 billion

- Operating Income = $2.5 billion

- Taxes @ 3% = $75 million

- EPS = $2.43 billion/1.22 billion shares = $1.99

The actual EPS far exceeds our original target of closer to a $1.75 level due to the forecasted smaller 3% tax rate.

Takeaway

The key investor takeaway is that AMD generated Q4 numbers and 2020 guidance that were good enough to keep the stock around $50, but the conservative projections on the exit rate will rally the bears. The company will need to beat their internal guidance to generate solid stock returns this year, but AMD has the products and the analyst skepticism on the earnings call confirms the conservative guidance positions the chip company for a boost to yearly targets.

AMD remains a stock to buy on dips. After the initial dip to $47, the stock trades below 25x forward EPS estimates whether the chip company achieves a $2 EPS in 2020 or 2021.

Looking for even more? Join DIY Value Investing.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: The information contained herein is for informational purposes only. Nothing in this article should be taken as a solicitation to purchase or sell securities. Before buying or selling any stock you should do your own research and reach your own conclusion or consult a financial advisor. Investing includes risks, including loss of principal.